Can Tailwinds Offset Current Headwinds?

With every day there is new, and significant, information for consumers and companies to digest. There is so much to potentially focus on that could derail the markets, in the short-term at least, with the U.S. war with Iran plus the continued Russia-Ukraine War heightening tensions domestically. Most are grappling with how to digest one major event to the next. Yet, markets have remained quite steadfast.

Notwithstanding the market detraction throughout March, the U.S. markets were down quite modestly from where they ended 2025. One tailwind that is supporting the markets is the continued A.I. boom – several large-cap technology companies have pared back gains from recent years, but it is interesting to see the rally broaden out to small- and mid-sized companies. The massive initial investments in A.I. were expected to trickle down at some point (given that small companies cannot cut $100 MM checks to create a proprietary A.I. tool), but adoption seems to already be reaching more mainstream avenues as development rapidly ensues.

A powerful wave that continued from 2025 was that diversification provided a stabilizing force for globally-diversified portfolios into 2026 – a ballast that was well supported with international investments last year. U.S. large-companies were broadly down about 4% year-to-date while U.S. small-cap stocks eked out a positive return for the quarter and were up 3.5%. International markets continued to post strong results even after the monumental rise in 2025. It wasn’t all roses though since international markets did experience a bit of an interim setback during the quarter. International stocks were up double digits through February, so the declines in March hit them relatively hard, but they still ended the quarter better than most U.S. stocks – being down 0.7% for the developed world and only down 0.2% for emerging markets.

Many cryptocurrencies struggled since most did not provide any solace to a downward trending market – Bitcoin was down over 22% year-to-date, not to mention being down 40% in the last six months. We remain cautious and unclear on cryptocurrency’s role, but short-term movements do not necessarily extrapolate to long-term results. Speculative and concentrated holdings – including evaluating an individual stock or cryptocurrency – can often deviate quite materially from what some might perceive as “fair value” in the short-term. Even the likes of the current Magnificent 7 stocks in the U.S. have each had points of being down 50%+ in the short-term. Diversification and a balanced portfolio are what we believe helps protect investors who are looking to retain, and build, their wealth over time since it can help smooth out the times when a stock’s fall may not get to see the light of day again.

Read on as we explore A.I. as well as the whether energy prices could be a boon for the economy over this cycle.

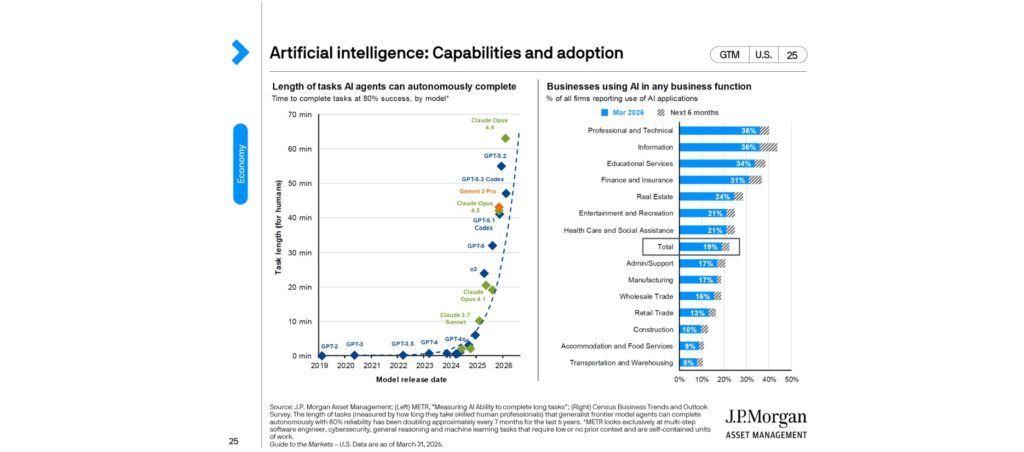

A.I. – how is it impacting your personal and professional life?

A.I. is one of the continued tailwinds that has provided a favorable offset to the headwinds facing consumers and businesses. The chart below is an interesting adoption perspective on what sectors of the economy are utilizing A.I. in any aspect of their business and their projected change in usage in the next six months. It’s beyond the scope of the newsletter to discuss whether, how, or why/if someone should be using A.I., but the chart on the left is a clear indication on why its use has already proliferated so quickly.

The meteoric rise in the length of time many of the top A.I. computing tools can now successfully operate is astonishing. It very much models the logarithmic scale many anticipated on the capabilities. We remain advocates for finding ways to BE the strategic thinker in the driver seat (maybe we should get a different metaphor with driverless vehicles no longer a thing of sci-fi…) , but to explore ways to offload some of the heavy lifting/analysis and data crunching to some of the A.I. tools. It’s worth noting that the base-line above is set at an 80% success rate as the threshold, so it’s ever more important to watch for computing hallucinations that sound real (all the more reason to keep a human involved with interpreting and providing direction on running things down further that don’t just sound right). A.I. is doing a phenomenal job of sounding quite compelling and good, even if it is flat out wrong. Be sure to keep your critical thinking hat on to try and spot something that doesn’t sound quite right.

Could energy prices be a boon? Plus Interest Rates!

The war with Iran is one factor that could derail the economy with gas prices hitting consumers’ directly in the short-term – a tough thing to overcome for cash flow for millions of Americans. However, one boon to the economy overall is that the U.S. is actually a net-exporter of total petroleum (since 2020), so higher energy prices could eventually (key word) benefit the economy for the first time in over 70 years. To see the benefit though, it’s likely to take some time to trickle down within the economy as compared to the near-instant impact that it hits consumers’ pocketbooks in the short-term. But, given that dynamic in the economy, it’s not entirely surprising the U.S. stock market hasn’t reacted more negatively to the spike in energy prices.

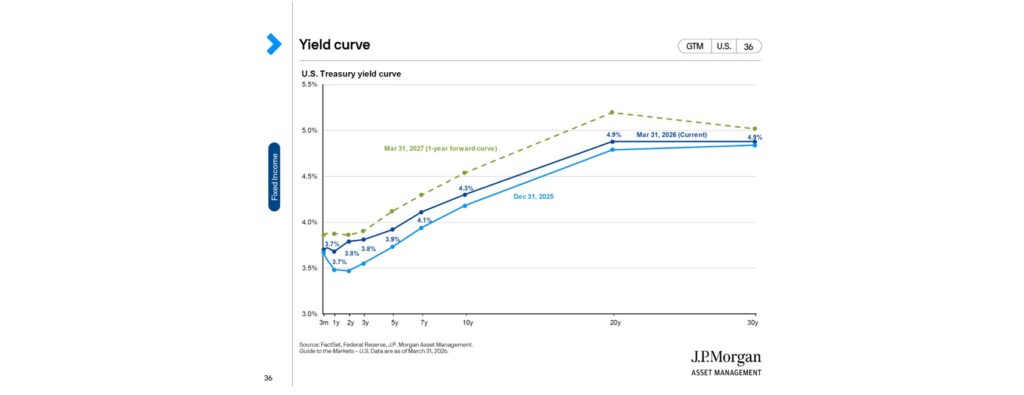

Interest rates are finally looking “normal” by historical standards. Below is an excerpted chart showing the yield curve – essentially what current interest rates look like from very short-term 3 month rates all the way up to 30 year rates. In most environments, you would typically expect to see higher rates for longer-term since in most instances there is a higher opportunity cost for lending out money for a longer period of time. It’s been a number of years since almost all portions of the yield curve were upward sloping (the March 31, 2026 dark blue line). Even still, 1 year rates are actually lower than 3 month rates, but all other components are similar to the traditional upward sloping yield curve that we’ve been accustomed to for decades (outside of the occasional hiccups where short-term rates often surpass longer-term rates in anticipation of a recession). After cutting rates to the 3.5-3.75% range in 2025, the Fed remained steady in March. Given current economic conditions, the Fed anticipates one rate cut in 2026 with the potential for no rate cuts during the year, so it is largely expected for interest rates to remain relatively flat-to-unchanged during the year.

We continue to see a bit of a disconnect between what is happening on Main Street with small companies that drive the economy at large vs. Wall Street for what is happening within large-public companies that have a heavy technology sector leaning. Lower borrowing costs in particular help mega-caps. And, another example recently of where the economy at large can have difficulties that are not necessarily reflected by what public stock markets are doing.

CLOSING REMARKS

Stock markets attempt to evaluate new-news in the context of future decades of earnings and expectations, so short-term news can cause seemingly large-scale swings in current prices given differences in how people may interpret the change in trajectory of the markets for years into the future. However, negative news tends to have an outsized short-term impact in the markets until the long-term lens can come into better focus. Historically, market forecasters tend to overshoot their projections (on the upside and downside) in the short-term, but consistently over decades, prognosticators tend to under-shoot the positive impact to markets when there has been ample time to process the news, adjust course, and adapt a strategy. But, short-term news and market gyrations can make compelling outcomes for opportunistic individuals who have appropriately planned for liquidity and cash flow (i.e. enough contingencies for “what could go wrong” (via Plan B, C, and D), if they can meaningfully reduce the scenarios of having to be a forced seller in a time of crisis and can instead be ready (and available) to take advantage of market opportunities that may crop up. It’s by having that discipline to put capital to work in stressed markets and not succumbing to selling-pressure that often help to build long-term wealth.

Interest rates have spent the last four years on a downward trajectory, and it’s unexpected that rates would meaningfully decline (or increase from here), so we may have found our “new normal” from the zero-bound range we had been accustomed to coming out of the Global Financial Crisis. Debt servicing and financing activity may be more manageable in the context of today’s rates – particularly with the mechanism of such inexpensive, heavy computing power and analysis tools available with A.I. to help bring down total investment costs for a lot of small businesses and consumers in today’s environment.

We remain cautious in our view of markets as they waffle between significant geopolitical headwinds with seemingly oppositely-supporting tailwinds of technology. Valuations aren’t screaming dramatic buying opportunities – nor were they in March’s sell-off. Over the last 100 years in the public stock market, there is on average a 10% correction that happens at least once per year, yet with all that is going on, the recent market rout did not even hit “correction” territory (close to it at almost 9% from the peaks in February), but hardly out of the norm for what is expected to happen at some point during each year.

Of course, any well-built strategy should factor in the trading costs and tax impact of any adjustments – sometimes a difficult hurdle to warrant any large-scale shift. We remain alert for any tax-loss-harvesting opportunities that could open up – to make lemonade out of lemons – but not as a mechanism to “get out of the way” of market movements. The markets have historically been quite humbling for their ability to outgrow even some of the worst of the news.